Life Insurance Basics

Term vs. whole life insurance: What’s the difference?

Term life vs. whole life: Coverage comparison

Below is a quick overview of common term and whole life policy differences, including a cost comparison for 35-year-olds.

|

Policy features |

Term life insurance |

Whole life insurance |

|---|---|---|

|

Duration |

10 to 30 years |

Life |

|

Cost |

$25 to $30/month |

$481 to $571/month |

|

Guaranteed death benefit |

Yes |

Yes |

|

Guaranteed cash value |

No |

Yes |

|

How cash value grows |

N/A |

Earns interest at a fixed rate |

|

Premiums |

Level |

Level |

|

Risks |

No cash value savings option |

Low interest rates and high premiums |

Methodology: Estimated term and whole life insurance quotes based on policies offered by Policygenius in March 2022 from our 10 partner life insurance companies: AIG, Banner, Brighthouse, Lincoln, Mutual of Omaha, Pacific Life, Protective, Prudential, SBLI, and Transamerica. Rates are calculated based on a $500,000, 20-year term life insurance policy and $500,000 whole life insurance policy paid up at age 99 for 35-year-old female and male non-smokers in a Preferred health classification.

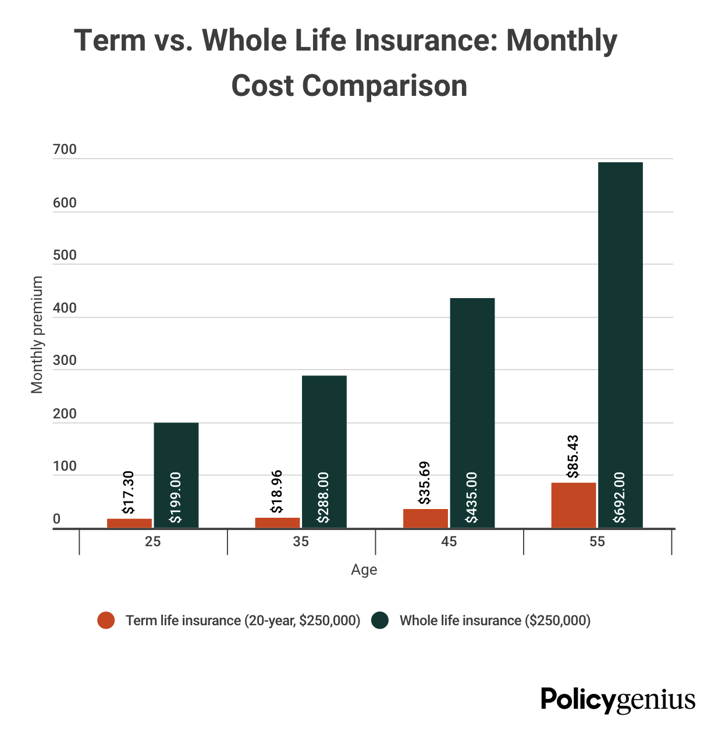

Cost comparisons for whole vs. term life insurance

Both term life and whole life premiums stay the same for the duration of an insured's policy. Because coverage lasts longer and comes with a cash value, whole life insurance is five to 15 times more expensive than a comparable term life policy.

The charts below compare the monthly cost of a $250,000, 20-year term policy, and a $250,000 whole life policy for a male non-smoker at different ages.

|

Age |

Term life |

Whole life |

|---|---|---|

|

25 |

$17.22 |

$199.00 |

|

35 |

$18.95 |

$288.00 |

|

45 |

$35.72 |

$435.00 |

|

55 |

$85.40 |

$692.00 |

Note that a whole life policy costs as much as 15 times more than term life in the example above for the same death benefit. Visualized another way, the difference in cost is even clearer:

Methodology: Quotes based on policies for male non-smokers in a Preferred health classification, offered by Policygenius in March 2022 from our 10 partner life insurance companies: AIG, Banner, Brighthouse, Lincoln, Mutual of Omaha, Pacific Life, Protective, Prudential, SBLI, and Transamerica. Rates are calculated based on a $250,000, 20-year term life insurance policy and $250,000 whole life insurance policy paid up at age 99 for a 35-year-old male non-smoker in a Preferred health classification.

How to choose between whole life and term life insurance

Whether your client needs a term life or whole life policy depends on their financial needs.

-

Term life is right for your client if: They want an affordable way to leave a death benefit behind to financially support their loved ones and they expect to self-insure in the future

-

Whole life is right for your client if: They want to minimize their estate tax, they want to build cash value, or they have long-term dependents

Term life insurance is the right life insurance policy in most cases because it offers the same amount of death benefit as whole life insurance for a fraction of the price.