Life Insurance Basics

What are life insurance classifications?

When a proposed insured (PI) applies for life insurance, they are assigned a health classification based on their application details. If they present fewer insurance risks — like complex health conditions, risky habits, or dangerous hobbies — they'll get a better classification and more affordable rates than someone who raises some flags.

Life insurance companies use roughly the same four classifications to determine an individual's premiums. But, each company varies slightly in how they assign those classifications. For example, while it’s common to receive a lower classification for any tobacco use, some providers give infrequent cigar smokers a better classification than casual cigarette smokers.

What are the different health classifications?

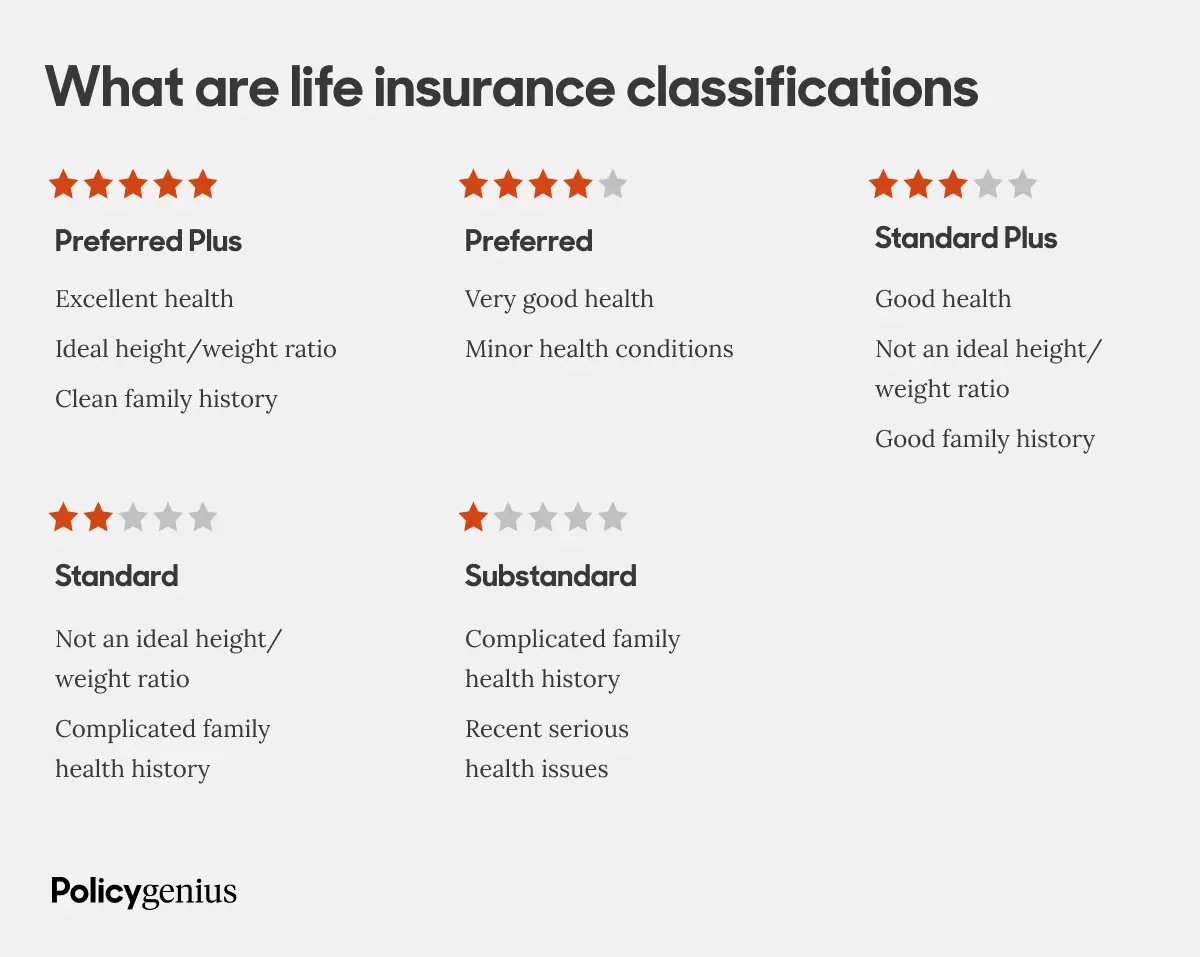

The four life insurance health classifications are:

-

Preferred Plus

-

Preferred

-

Standard Plus

-

Standard

People with more complex medical histories may fall into a broader category called Substandard or Table ratings. Providers also have health classifications exclusively for smokers, which come with significantly higher rates.

Preferred Plus

Sometimes called Preferred Elite, Super Preferred, or Preferred Select, this is the best classification a PI can get and comes with the lowest premiums. It means the PI is in excellent health, their height-to-weight ratio falls into the insurance company’s desired range, and their family history is as squeaky clean as their lifestyle.

Preferred

Outside of a few minor factors, like high cholesterol or high blood pressure, the PI is in very good health. They won’t get Preferred Plus rates, but their premiums will still be very competitive.

Standard Plus

The PI is in good health, but they might have a few outliers to keep an eye on or their height-to-weight ratio doesn’t fall into the insurer’s range for Preferred classifications. Their family history is unremarkable, so they shouldn’t have any surprises in their future.

Standard

A common difference between Standard and Standard Plus is that the individual's family history plays a role, and their family members probably had medical issues before age 60. They will see higher life insurance premiums in this class, but they're still able to get insured.

Table ratings

This isn’t a specific rating classification like the others; instead, based on an individual's health history, they're placed in the Substandard category, which is graded by either letters or numbers (typically A to J or 1 to 10). This reflects a complicated health history or recent health issues, such as a heart attack.

The PI's premium will, on average, be the Standard price plus 25% for every level down the table ratings:

-

A = Standard + 25%

-

B = Standard + 50%

-

C = Standard + 75%

-

D = Standard + 100%

-

E = Standard + 125%

-

F = Standard + 150%

-

G = Standard + 175%

-

H = Standard + 200%

-

I = Standard + 225%

-

J = Standard + 250%

The PI could pay an extra 250% on their premiums at a Table J/Table 10 health classification, which isn’t ideal. But they can still get insured and provide for their dependents when they die.